What is a Business Line of Credit? Why Does Your Business Need One or More? How do you Qualify for a Business Line of Credit? Let’s find out together!

What is a Business Line of Credit?

A business line of credit is the most flexible and useful unsecured financing available. They offer easily accessible cash and typically have low interest rates.

Best of all, your business line of credit can be used over and over with monthly payments typically calculated at 2% to 3% of the balance. Of course you only pay on the balance of the line of credit that you have utilized.

Why Does Your Business Need a Business Line of Credit?

One thing is certain in every business – cash flow fluctuates. You may enjoy periods where cash if flush and you can accomplish anything you desire in your business.

But if your business is like the majority of small businesses (61%) who struggle with cash flow or the nearly a third (32%) unable to either pay vendors, pay back pending loans, or pay themselves or their employees due to cash flow issues, a business line of credit provides the safety net for your business to survive and thrive.

How Do You Qualify for a Business Line of Credit?

A business line of credit, like any business loan application, is evaluated on Three Pillars – your personal credit, your business credit and your business financials.

Personal Credit

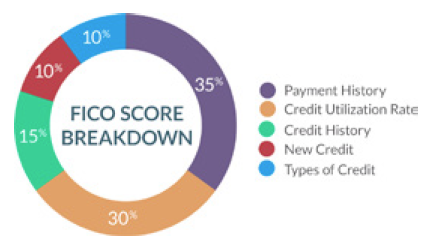

Have you ever wondered how your credit score is determined? There are five factors considered by the credit reporting agencies – Experian, Equifax and Transunion:

35% Payment History

35% Payment History

• Timing of delinquencies – was it last month or 3 years ago.

• Level of delinquencies – 30, 60, 90, 120 days late.

• Last activity date.

30% Amount Owed

• What is your total debt?

• How many accounts with balances?

• What is your overall installment and revolving utilization?

• What is your individual account utilization?

15% Length of Credit History

• How old is the oldest account?

• What is the average age of accounts?

• What is the mix of newer or older accounts?

10% Mix of Credit

• What kind of credit do you have in your file – mortgages, credit cards, loans, etc?

• The combination of credit – all the same type of credit does not look as favorably as a healthy combination of different types.

10% Inquiries

• How much new credit are you acquiring?

• The time interval between each new credit acquired – acquiring many new credit cards or loans in a short time can affect your score negatively.

• How many new accounts are on file?

FICO Scores range from 300 to 850.:

FICO Scores range from 300 to 850.:

- Excellent: 760-850

- Very Good: 700-759

- Good: 660-699

- Fair: 620-659

- Poor: 580-619

- Very Poor: 500-579

- Horrible: Less than 500

Your FICO score can be a very important consideration to qualify for a business line of credit. If you carefully manage your payment history, credit utilization, credit history, mix of credit and inquiries, you can improve your personal credit score.

Business Credit

There are three business credit reporting agencies – Dun & Bradstreet, Experian Business and Equifax Small Business. While personal credit scores range from 300 to 850, business credit scores range from 0 to 100. A higher score is an indicator of your business credit worthiness.

Dun & Bradstreet

D&B uses a Paydex score that ranges from 1 to 100—the higher the number, the better shape your business’s credit is in. D&B looks at one specific factor to calculate your business credit score – how timely you are when paying vendors? It is important to pay your debts early so your vendors report a good history of payment to raise your business credit score.

Experian

Experian calculates your business credit score based on your credit obligation from lenders and suppliers, any legal filings for your business, and background information about your business. The Experian credit report is called the “Intelliscore Plus” and is also based on a score from 1-100. Additionally, an Experian business credit score includes a risk classification from 1-5, with 1 being the least risky.

Equifax

Equifax collects information about your business and evaluates your payment trends, business credit history, public record and demographics. Their business credit report gives you three scores—a payment index score, a credit risk score, and a failure risk score.

Business Financials

In order to qualify for a business line of credit, your business financial history and current situation will be closely scrutinized by any lender. The starting point always begins with a close look at your business legal documentation. In addition, lenders will review your business financials. tax returns, trade references and bank references.

In order to qualify for a business line of credit, your business financial history and current situation will be closely scrutinized by any lender. The starting point always begins with a close look at your business legal documentation. In addition, lenders will review your business financials. tax returns, trade references and bank references.

Your business financial review will require two years of financial statements, including your balance sheet and income statement, also often called your profit & loss or P & L statement. Your balance sheet should accurately reflect your assets, liabilities and equity on a specific date, usually the end of a month, quarter or year, while your income statement should detail your revenue, expenses and net profits over a period of time, usually a calendar year reported on a monthly basis.

In addition to annual financial statements for the past two full calendar years, you should also prepare year-to-date financial statements for the most current month when applying for a business line of credit.

Tax Returns

You will need to submit the most recent two years of business tax returns. Although it may be beneficial to report operating losses on your tax returns to minimize your tax liability, you will need to show profits on your business tax returns to qualify for a business line of credit.

Trade References

You will need a minimum of five trade references that have provided credit to your business and report a favorable credit history. Although this can be a challenging step in building your business credit, the sooner you start, the sooner you will be able to qualify for a business line of credit.

Bank References

Of course you will need a minimum of one bank reference to qualify for a business line of credit. Your business bank account should be at least two years old and have an average daily balance of $10,000 or more during the past three months.

Get Started

A business line of credit is the most flexible and useful unsecured financing available, offering easily accessible cash and typically low interest rates. If you are like most businesses, your cash flow fluctuates. A business line of credit is a great way to manage your business through the peaks and valleys.