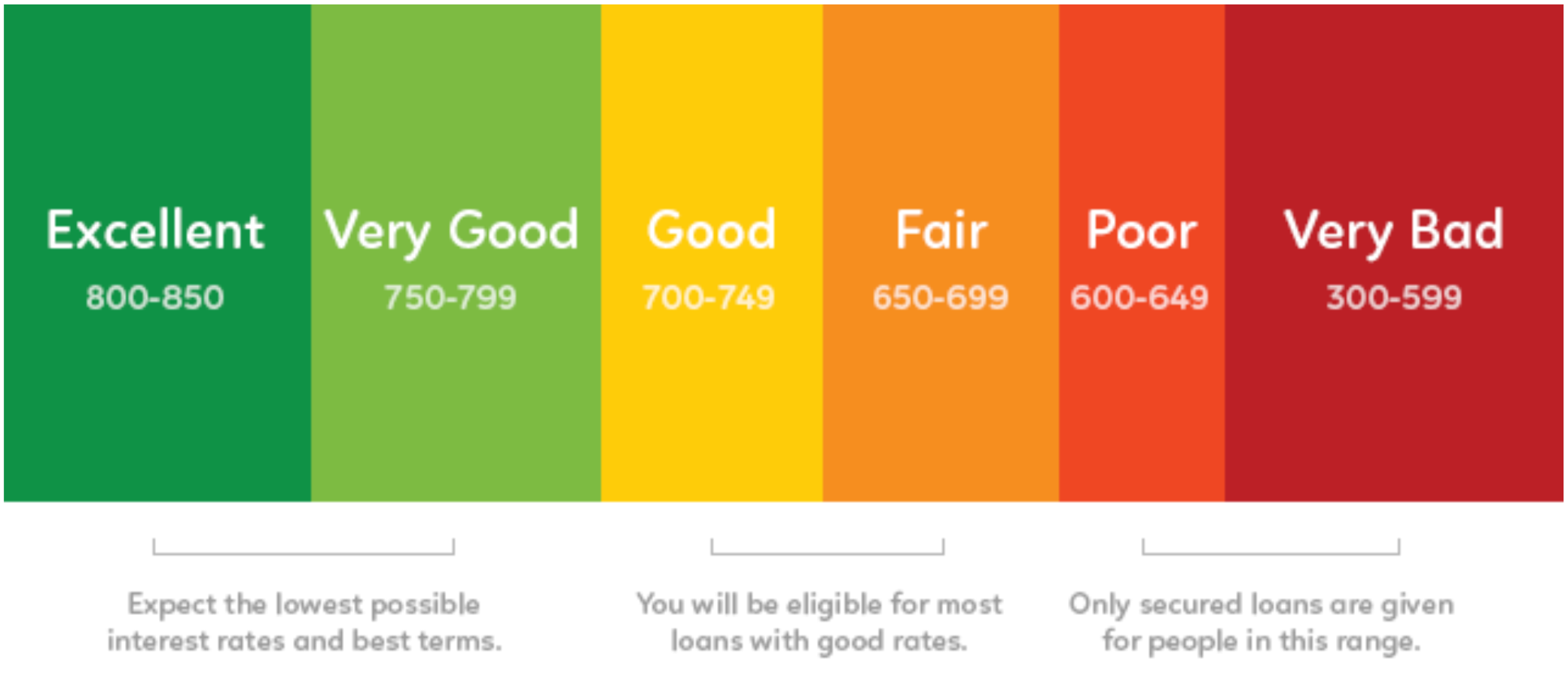

We live in an age where it is very important to understand your personal credit score. Your credit score can determine where you live, where you work, your insurance premiums, loans, credit cards, mortgages and bank accounts. This three digit number literally can change your life depending on how high or low it is. With so much on the line, why settle for anything else than the perfect credit formula?

There are two different types of trade lines on a credit report – positive and negative. A positive trade line is any type that will

increase your credit score and allow you to receive credit in the future. A negative trade line is a negative item or derogatory item on your

credit report and can lower your credit score.

Why Your Personal Credit Score Matters

OK, so you have your credit report…. but what exactly does everything on the credit report mean?

There are so many terms on a credit report that can be confusing or even intimidating – but they don’t have to be! All you have to do is learn what those terms mean. Once you are educated on your credit report, it will be easier to find out if your credit report data is inaccurate.

Remember, credit reporting bureaus make money whether the information is accurate or not, so get smart and find out the facts about your personal credit score.

Revolving Accounts

A revolving account is basically another name for a credit card account. It is called revolving because the full balance does not have to be paid

each month – only a minimum balance set by the creditor. If there is a high outstanding balance, it is transferred over to the next month.

However, if the minimum is not paid, a late charge is placed on the account which greatly damages your credit score. Also running a card

to its limit looks bad on your credit report because it shows that you may have a problem paying your debt off. The best thing to do is to

make a charge and pay it off in full as soon as you receive the bill from the creditor.

Not only will this look good on your personal credit score, but it will save you from paying money in interest.

Closed and Inactive Accounts

Accounts that you have had in the past that that you no longer use do not count in your credit score and are considered inactive accounts. A closed account has either been closed the creditor or the consumer themselves.

It used to be that when a creditor closed your account it was more damaging to your credit report than if you did it yourself as the consumer. With newer scoring models, it does not matter who closes the account, you or the creditor, it still affects the score.

Late Payments

Late payments are one of the most common things to find on a credit report, but also the hardest thing to dispute. A thirty day late payment

can significantly lower your score, and hinder your chances of getting credit cards in the future, because it shows that you have trouble making payments.

It makes little difference whether you pay the minimum or the full balance, as long as you make the payment on time and you have not over utilized the account. However, the best thing to do is always pay your full balance to avoid any problems with debt in the future and protect your personal credit score.

Charge-Offs

A Charge off is an account that has been so overdue that they write it off as non-collectible. Usually these accounts come from credit card accounts, medical bills, utility bills, loans or any type of account that is not paid on time.

Charge offs can remain on your credit report for up to 7 years from the 30-day delinquency that sent you into the charge off. This is not something potential lenders want to see because this shows that you never paid your debt, and you may do the same thing with the money you borrow from them.

The smartest thing to do is to pay your past due amount before it becomes a late payment or a charged off account to ensure you will receive credit in the future and avoid damaging your personal credit score.

Collection Accounts

A collection account is an account sent from a creditor to an outside agency or its own collection agency in order to collect an unpaid debt.

After an account is charged off, it usually will go into collections, because they still want to receive money for the debt. This account can now be on your credit report in two places, listed as a charge off with the original creditor and as a collection with the collection agency.

It is always better to pay a charge off or collection account rather than to leave it as unpaid. On a credit report there are “paid collections” and “unpaid collections.”

When disputing information on your credit report, if you have documentation that you have paid a collection or charge off account, it should state that on your credit report. Creditors will see this and note that even though you were late making the payment, at least it is paid.

However, some creditors will reject a potential borrower just for having a collection account or charge off on their credit report, so always pay bills on time!

Inquiries

At the end of every credit report, there is a list of creditor names who have requested your credit report recently. It is better to have fewer inquiries because it shows that you are applying for less credit, and more inquiries could indicate a potential bad situation to lenders.

Each inquiry stays on your credit report for 2 years and could damage your credit.

Mortgage Foreclosures

A mortgage is a loan a person takes out to purchase their home and is one of the most significant trade lines on a credit report.

When a lender looks at how a person paid their mortgage, they look at how many late payments there were and if the home went into foreclosure. If a home goes into foreclosure, it shows that the person simply was not paying their mortgage or could not afford their mortgage.

This is a major derogatory and one of the worst things to have on a credit report, and will remain on your credit for 7 years. However, there is a simple solution to having a foreclosure on your credit report. Either pay the mortgage on time, or dispute it with the credit reporting agencies. A lot of the time, they report the information inaccurately, and can damage someone’s entire life.

Summary

As you can see, many factors are considered in determining your personal credit score. The best path is to manage your credit wisely and avoid closed accounts, late payments, charge-offs, collection accounts, inquiries and mortgage foreclosures.